Postal Savings Bank of China meets the “10 times speed” of financial technology

“Disruptive technologies often come from outside intrusion or innovation.” This is an insight mentioned many times by Kevin Kelly, author of the best-selling book “Out of Control”.

There are countless similar cases. What impacted Google was not a search engine, but ChatGPT; it was not the car peers that overturned the fuel vehicle giant, but the “new species” Tesla. In the technology industry, this strategic turning point has been given a term called “10x speed”.

There is no doubt that the current banking industry is also facing its own “10x speed” variable, which is the revolution brought about by financial technology. In the face of “10 times faster” change, what kind of concentration and action should be maintained? How can the strong be stronger? This is something that many banks need to think deeply about.

Whoever can take the initiative to speed up reform-style innovation, “destructive creation” of the traditional business model, and carry out a profound change from thought to action, from the top to the grassroots, and from the inside out, will have a greater chance to stand out.

Large banks that have been at the forefront of previous information revolutions have stronger strength and greater courage to change, and are more motivated to run at the same “acceleration” as Internet giants.

01

Big state-owned banks run out of digital financial “acceleration”

The word “subversion” is always hidden in the long river of time.

In the past 20 years, the new technological revolution has achieved unprecedented leaps. For example, the maximum speed of supercomputers has increased by more than 800 million times, the capacity of mechanical hard disks has increased by 20,000 times, and the wireless speed has increased by 4,000 times.

In the banking industry, new technologies are driving unprecedented changes in the business model, industry ecology and competition landscape. To some extent, the competition of a bank in the future will mainly be the competition of technological capabilities. According to McKinsey’s research, in order to win the technological war, the world’s leading banks have invested nearly one-fifth of their pre-tax profits and human resources in the research and development of disruptive technologies.

From a domestic perspective, there is a view that the digital transformation of joint-stock banks is faster, while state-owned large banks are more difficult to turn around digitally due to their larger size. But in fact, this status quo has undergone earth-shaking changes, and the digital layout of major state-owned banks is subverting the industry’s previous cognition.

“Science and technology innovation is a ‘key variable’ and also the ‘biggest increment’ for high-quality development.” Liu Jianjun, President of Postal Savings Bank of China, said that Postal Savings Bank has always adhered to “technology-based development” and adhered to the concept of achieving high-level technological self-reliance and self-improvement. Continue to increase investment in financial technology innovation, fully promote the empowerment of financial technology, continue to improve the level of financial services, and inject strong technological momentum into the digital transformation and high-quality development of Postal Savings Bank.

As one of the six major banks, in recent years, Postal Savings Bank has launched a series of major financial technology reforms, which have attracted the attention of the industry due to their strength, scope, speed, and industry leadership. A new game-changer in financial technology.

“If the development of digital finance is compared to a forerunner running forward, then strategic deployment, technology leadership, and data drive are the three core ‘organs’ that provide the driving force. Postal Savings Bank has clear goals, strengthens the body, and releases kinetic energy. There is ‘acceleration’ in financial development.” Liu Jianjun said.

Strategy first, occupying the high ground of financial technology, digital transformation has long been a key strategy of Postal Savings Bank. Postal Savings Bank of China has planned the “123456” digital strategic layout,Among them, “1” is to adhere to the “one main line” of digital ecological bank transformation; “2” is to promote the two tracks of “digital business model innovation” and “intelligent reshaping of traditional banks” in parallel; “3” is to implement personal finance and corporate finance “4” is to create four major digital capabilities: product innovation, risk prevention and control, data empowerment and technology leadership; “5” is to focus on breaking through the five major areas of ecology, channels, products, operations and management ; “6” is to strengthen the top-level design, coordination mechanism, agile organization, expert team, resource guarantee and assessment incentives.At the same time, Postal Savings Bank alsoPromote the implementation of the “SPEED” technology strategy of intelligence, platform, experience, ecology and digitalization.

Although Postal Savings Bank of China has a century-old foundation, it is a young bank. Dare to dance with the times,Recently, Postal Savings Bank of China has also released a series of financial technology strategic layout.

The first is to “replace the engine”. Postal Savings Bank launched four new-generation systems: personal business core system, corporate business core system, credit card core system, and mobile banking. Recently, the core system of the new generation of personal business has completed the no-feeling migration of more than 650 million personal customers, which means that the core system of the new generation of personal business has been fully put into production.

Nearly 1,400 days and nights, tens of millions of lines of code development, invested thousands of business and technical backbonesa new generation of personal business core systemCan satisfy over 650 million customers across the bank,The support and services of nearly 40,000 outlets,It can also meet the needs of the rapid development of Postal Savings Bank’s business.Postal Savings Bank’s new generation personal business core system can be described asA “hard core work” for technological breakthroughs.

As we all know, the core system is the top priority of a bank’s IT system construction, the brain and heart of a bank, and an important manifestation of a bank’s technological strength. The reshaping of the core system is a huge and complex project, which includes not only the innovative application of certain new technologies, but also all-round digital transformation including business transformation and IT transformation.

At the beginning of the planning and design of the core system of the new generation of personal business, PSBC aimed at the frontier of new technology, based on the growth of PSBC’s business volume in the future, and set a goal of 3 billion transactions per day and 6 transactions per second.70,000pen target. At present, PSBC’s new-generation personal business core system has a peak load of 67,000 transactions per second, and according to the annual growth rate of transaction volume exceeding 10% in the past three years, it can fully meet the needs of business growth in the next 10 years.

According to Niu Xinzhuang, Chief Information Officer of PSBC, at present, PSBC’s new generation of personal business core system has become a powerful engine supporting the rapid development of PSBC’s business, giving wings to the bank’s operation management and digital transformation. Postal Savings Bank has developed and assembled nearly 5,000 “building block parts” that can be flexibly assembled, which can be combined and arranged according to different scenarios to support faster business innovation and better and faster support for business development.

The changes brought about by the new-generation personal business core system can be intuitively felt from the data.

Postal Savings Bank’s new-generation personal business core system has achieved outstanding results with a daily transaction volume of over 500 million transactions and a system success rate of over 99.99%; the average time spent on omni-channel online transactions has been shortened from 93 milliseconds to 65 milliseconds, a reduction of 30%; The end-of-day processing time was shortened from 273 minutes to 197 minutes, a 28% reduction; the total interest settlement time was shortened from 140 minutes to 25 minutes, a 82% reduction.

The launch of this system is the first in the industry.This is the first of a large bank to simultaneously adopt enterprise-class businessModeling and distributed micro-service architecture, a new generation of core system based on full-stack safe and controllable software and hardware, is an important practice of independent and controllable key technologies of financial technology in the domestic banking industry.

The second is long-term support for banking business innovation, which is inseparable from a group of leading fintech innovation platforms. Postal Savings Bank has built Postal Savings Brain AI platform, “Blockchain +”, cloud computing, big data and other platforms, and has realized hundreds of customer experience, credit business, digital RMB, intelligent customer service, intensive operation, risk prevention and control, etc. Scenario application, with rapid construction of application scenarios and technical output capabilities.

As an important plan of Postal Savings Bank in the field of artificial intelligence, “PSBC Brain” is the core achievement of Postal Savings Bank to build a foundation of digital intelligence. The intelligent outbound service that supports natural voice interaction covers consumer credit, marketing and other scenarios, touching Over 30 million customers.

New technologies are changing rapidly, requiring banks to always be at the forefront of new technologies. On February 16, Postal Savings Bank of China (PSBC) announced its access to Baidu’s “Wen Xin Yi Yan”, which is the first time that “Wen Xin Yi Yan” has been implemented in a large state-owned commercial bank. The combination of “PSBC Brain” and “Wen Xin Yi Yan” will further improve PSBC’s capabilities in areas such as generative artificial intelligence (AI), open dialogue, and cross-modal semantic understanding, and continuously improve the application of intelligent innovation efficiency.

At present, data capabilities have been elevated to a strategic level by banks, and it is imperative to increase the value of data assets. Postal Savings Bank’s big data platform integrates 146 important business systems in the bank, builds six major data marts including ten major financial themes, data models and customer risks, and more than 700 data services such as the white list of the industrial chain on the data center platform, allowing data Assets become the drivers of digital transformation.

The third is that the Postal Savings Bank insists on taking the road of independence and control.Key infrastructure construction “independent and controllable”It is not only the strategy of national digital development, but also an important foundation for the development of banks.

In the traditional impression, banks seem to have nothing to do with high technology, and now banks have become the wave of financial technology.Postal Savings Bank in the field of financial technologyIt can be seen that large banks are starting the “10 times” battle of technology with high investment and high cohesion.

02

Reconstructing the Super Platform: Enhancing Customer Value Creation and Experience

Big banks spend a lot of manpower and material resources to deploy financial technology. What is the ultimate goal?

Qu Jiawen, vice president of Postal Savings Bank of China, said, “Currently, the century-old situation is accelerating, and a new round of technological revolution and industrial transformation is in-depth development. For commercial banks, the development of digital finance will help promote the reshaping and upgrading of financial services and the transformation of enterprises. Transformation and development can also further empower the high-quality development of the real economy and continuously improve customer experience.”

Let’s look at a case. A customer wants to check the historical transaction details of the past 5 years from mobile banking. This seemingly “simple” service requirement is not easy for most banks. solved problem.

Recently, Postal Savings Bank officially released version 8.0 of mobile banking. The new version of mobile banking allows users to query transaction details over 8 years in real time.

“More than 3,000 servers, more than 100 sets of databases are running, and 1,024 data fragments have been made”, and the data of 650 million customers is fully processed, and the real-time response reaches the millisecond level. The powerful support of these financial technologies is hidden behind. What the front end shows to users is that with a single click, they can see the transaction details of the past 8 years, which really improves the experience.

Is such a function necessary? no. Does the bank have to do it? The answer is yes.

There are many indicators for evaluating a bank’s comprehensive and digital capabilities, but mobile banking is one of the most critical indicators when looking at a bank’s future capabilities. This is because mobile banking involves most of the bank’s departments and businesses, and is the ultimate manifestation of a bank’s comprehensive financial and digital capabilities.

Because of this, bank App update iterations are becoming more and more intensive. According to Analysys Qianfan data, as of mid-December 2022,2022In 2019, 70 banks updated their mobile banking App version 529 times. Three major state-owned banks, including Postal Savings Bank of China, launched version 8.0 of mobile banking. Mobile banking has become a bankThe main frontier for interacting with customers.

Among these mobile app iteration cases, the PSBC Mobile Banking 8.0 iteration is unprecedented.

Refactoring + experience.Fintech brings architectural restructuring to enhance customer experience and create more value for customersIt is the ultimate goal of fintech development.

Times are changing, technology is changing, and customer preferences are changing. In order to provide customers with safer, more convenient, more efficient, smarter and warmer financial services, Postal Savings Bank has been working hard. Based on this, Postal Savings Bank has restructured the mobile banking and achieved a new upgrade. It is understood thatPostal Savings Bank Mobile Banking 8.0 has upgraded hundreds of functions, with a total of over 1,400 function points.

Open mobile banking for more than 8 years of real-time query of transaction details, relying on independent research and development, industry-leading unified query system to achieve. Based on big data technology, it adopts a distributed architecture to build a flexible and scalable data model. Through data processing, it realizes historical data query and solves the performance bottleneck of traditional database mass data storage and mass data processing. It has good scalability. This is the powerful technological support brought by PSBC’s new generation personal business core system.

Mobile banking has become an important position for digital transformation and a concentrated expression of digital service capabilities. It is also a key platform for banks to reshape customer relationships and improve customer experience and stickiness.

In recent years, large international banks have generally realized that customer relations are crucial to the future survival of banks. BBVA, Citigroup, HSBC, ING, etc. generally regard “establishing a new type of intimate relationship with customers” as the “initial heart” of transformation. According to a research report by KPMG, two of the six state-owned banks have implanted “customer experience management” in their corporate strategy development.

By the end of 2022, the number of mobile banking customers of Postal Savings Bank of China has exceeded 344 million. How can mobile banking undertake the important task of banks to empower customers to create value and improve experience?

Postal Savings Bank attaches great importance to customer experience management, builds mobile banking as the main platform for personal customer interaction services, and constantly improves experience management. First, the business and technology departments of the head office have established dedicated customer experience teams to establish a quantifiable user experience evaluation system and a full-process experience optimization mechanism to continuously improve platform performance, enrich product functions, rationally layout interfaces, and optimize business processes; From the head office to each line and branch, there are part-time experiencers who are responsible for collecting customer feedback on a daily basis; third, based on customer complaints and daily feedback, to perceive customer service suggestions and pain points; fourth, to analyze online operations last year, Continuously improve and optimize customers’ mobile banking journey.

In terms of technological application innovation, the new generation of mobile banking 8.0 integrates face recognition,A number of technologies such as text recognition are integrated into key links such as login, transfer, wealth management, and credit, and multiple versions such as standards, youth, agriculture, wealth, and large-character versions are set up. Face” new look.

Technology has also brought platformization and intelligent means. Postal Savings Bank focuses on creating value for customers, and strengthens the integration of technological means and professional companionship in the process. For example, in 2022, the wealth management products sold by Postal Savings Bank’s mobile banking will be 2.7 trillion, accounting for 95.68% of wealth management sales, and customer recognition will continue to increase.

03

Intensify agile transformation, aiming at the strongest “technical capability”

Persist in taking the difficult and correct path, although you have to experience different hardships and ups and downs, but it will make you stronger.

Fintech is called the “second growth curve” and “second entrepreneurship” by many banks, and the competition for hegemony will definitely bring about changes in the banking industry. Although Postal Savings Bank’s financial technology started late, it has accelerated rapidly in recent years.In some fields, it surpassed many peers, relying on the substantial improvement of technological capabilities. The essence of financial technology is a war for talent and investment, and PSBC has invested heavily in this regard.

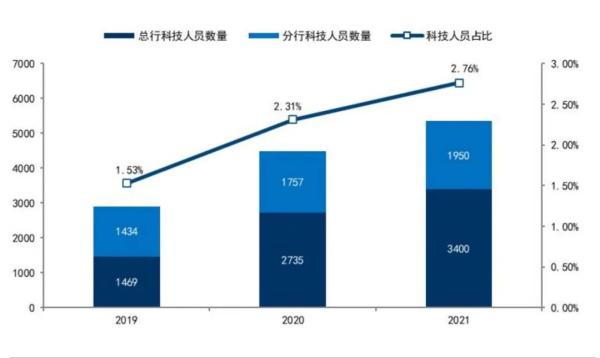

With these sets of data, in the past three years, the number of scientific and technological talents of Postal Savings Bank has increased by more than six times. From a few hundred in 2019, by the end of December 2022, the IT team of Postal Savings Bank’s head office has reached more than 4,300 people. More than 6,300 people, including the outsourcing team, the overall scale has reached 15,000 people; nearly 30 billion yuan has been invested in financial technology in the past three years, and the investment will be increased in the future.

Postal Savings Bank’s scientific and technological personnel continue to increase

Source: Company financial report, Guosen Securities Economic Research Institute

Postal Savings Bank has adopted a number of measures to effectively stimulate the enthusiasm and creativity of scientific and technological talents.for exampleFor the technology line, increase performance appraisal incentives; create a young and professional technology team, form 7 information technology sub-sequences such as structure and demand, and buildEstablish a three-level talent echelon of “youth, backbone, and leader”.

Under the guidance of new technologies, the talent building and system innovation of banks are undoubtedly full of challenges. With scientific and technological hard power and scientific and technological talents, how to let them integrate and explode with strong “scientific and technological capabilities”? The transformation of organizational structure is imperative, and the exploration of agile organizations is also accelerating.

Matching the organizational structure with the current needs is an important basis for the digital transformation of banks. In 2019, Postal Savings Bank carried out a thorough digital reconstruction, established the Financial Technology Innovation Department and the Data Management Department, and formed the IT governance structure of the head office “three departments and two centers” from the original “one department and two centers”; It has formed a “1+4+N” independent R&D system consisting of 1 head office R&D center, 4 sub-centers, and N branch R&D centers to accelerate the improvement of independent R&D capabilities.

In the past, the banking industry believed that the IT governance of “three departments and two centers” was very complicated. However, Postal Savings Bank has enjoyed the results brought about by the reform of IT governance. More and more specialized and refined.

In recent years, Postal Savings Bank has embarked on a unique path of technological innovation, which has been highly recognized by all parties.

But how do big businesses stay alive? The secret of Postal Savings Bank of China is to embed the concept of digitalization in the strategy and implementation of the company, set up a leading group for digital transformation to coordinate and promote related work, and improve decision-making efficiency through organizational guarantees.

Currently, Postal Savings Bank of China has established a “matrix-style” general-branch coordination system to give full play to its resource endowment in multiple points and areas, and promote the characteristic transformation and innovation practice of each branch. At the same time, all 36 tier-one branches of the bank have established digital transformation leadership groups to actively promote digital transformation within their jurisdictions, give play to regional characteristics and tap regional potential.

One of the key links in the deep integration of technology and business lies in the construction of an agile organization. In the past three years, Postal Savings Bank has continuously upgraded the integration of agile development and industry technology, built an agile R&D model in line with its own business development characteristics, greatly shortened the product delivery cycle, and better met the needs of business innovation and development and market competition .

The “small mobile banking team” is an important attempt of PSBC to explore agile transformation. According to the different characteristics of different sections of mobile banking, such as “My” and “Credit Card”, working groups were established respectively. The team members come from different fields such as development, testing, business, and demand analysis. The combination of vertical and horizontal management can not only improve efficiency, but also ensure project quality.

“The biggest gain from agile research and development is the integration of business and technology, and in the process of integration, we have realized the empowerment and innovation of business. What we didn’t dare to think about before, we have the courage to think and do it through trying, and do it through trying again and again. Better and more successful.” Xu Chaohui, chief engineer of Postal Savings Bank, revealed that since last year, Postal Savings Bank has upgraded the integration of agile development and industry technology, making the organizational form more flexible and the output efficiency more efficient.

At present, the agile culture of Postal Savings Bank of China has been at the forefront of major banks. If the realization of digital transformation is to promote bank reform at the level of productivity, then building an agile organization is to provide continuous support and guarantee for digital transformation at the level of production relations.

In the future, Postal Savings Bank will continue to explore, integrate the technology team into the business department, extract the common content of business needs, push the integration of business and technology in depth, and effectively improve the level of technology empowerment. It can be said that PSBC has blazed a path with its own characteristics, whether it is the change of organizational structure or the transformation of agile organization.

04

Bank of the Future: Refining a Fintech Industry

Almost any industry cannot escape the reincarnation of the enterprise life cycle theory.

The same goes for innovators in banking. Guosen Securities found that1990sThe U.S. banking industry began to transform in the early 1990s. After several years of survival of the fittest, most of the winning banks have adjusted their business scope and organizational structure, and continued to increase their innovation efforts.

If you want not to be eliminated, you need to be the ever-changing winner. In the future, the development of banks will depend more on financial technology innovation. Whoever can take the lead in deploying financial technology innovation and continue to make efforts will seize the opportunity and accelerate the realization of high-quality development.

Looking back on the past, the information technology of Postal Savings Bank has also gone through an extraordinary course.Going through five stages of development: start-up, unified version, 09 plan, “13th Five-Year” IT plan, and “14th Five-Year” IT planGradually embarked on a road of financial technology innovation with unique PSBC characteristics.

More importantly, through digital reforms in the past few years, Postal Savings Bank’s digital transformation and innovation capabilities have been improved in an all-round way. Postal Savings Bank collided with innovative ideas through cross-line and cross-institution synergy and integration, created a transformation culture, and accumulated transformation forces. The atmosphere of “everyone actively participates in the transformation, and everyone actively plans the transformation”.

Postal Savings Bank’s digital reform and innovation have received the attention and recognition of third parties.

The research report of Guosen Securities pointed out that “PSBC’s young and high-quality workforce fully reflects the characteristics of being the youngest major bank, which will help PSBC accelerate the pace of innovation and release transformation dividends.”

In terms of remuneration, Postal Savings Bank has continuously improved its incentive system with market competitiveness. “PSBC has optimized the personnel selection and employment mechanism, fully stimulated the vitality of the organization, and has great potential.”

Compared with its peers, PSBC’s special resource endowment endows it with new room for imagination.The most unique value of Postal Savings Bank is rooted in the vast land of China, relying on extensive postal servicesIn terms of agency outlets, PSBC’s county-level outlets accounted for 70% of the total for many years, and the central and western regions accounted for 55% of the total, ranking first among major banks.

In the future, if Postal Savings Bank can open up the online and offline channels of the entire rural revitalization and provide integrated financial services for the vast number of urban and rural customers, it will exert greater value.

Since its establishment, Postal Savings Bank has always adhered to the retail banking strategy and created a series of distinctive labels. In the process of moving towards a digital ecological bank, it requires extraordinary courage, courage and patience to face challenges, promote the financial technology revolution, and wait for the bank to bloom new vitality in the future.

“The eyes are full of vitality and transformation, and the workers of the sky are striving for newness day by day.” In the future, financial technology will be the engine for banks to go to the sea of stars. Through a series of major changes, the round of “fission” innovation brought by financial technology to Postal Savings Bank has just begun. From a well-known big retail bank to a big bank with distinctive financial technology characteristics, the investment value of Postal Savings Bank will also be revalued.

This giant is taking off.